Replacement Cost vs.

Agreed Roof Payment Schedule

Which Roof Coverage Is Better for Arkansas Homeowners?

Most homeowners assume that if their policy says “Replacement Cost,” they’ll automatically receive a brand-new roof after a storm.

Unfortunately, that’s not always how roof claims work.

Understanding how your roof is actually insured before you have a claim can make a difference of thousands of dollars.

Make Cribb Insurance Your Google Preferred Source

Get helpful insurance tips, answers, and updates from a trusted Arkansas insurance agency.

Why Every Arkansas Homeowner Should Read This

Roof coverage has quietly become one of the biggest changes in homeowners insurance over the last decade.

As hail storms, tornadoes, straight-line winds, and roofing costs have increased across Arkansas, insurance companies have introduced new ways to settle roof claims.

Today, your roof may be insured under one of three different settlement methods:

- Replacement Cost

- Actual Cash Value, often called ACV

- Agreed Roof Payment Schedule

Most homeowners don’t discover which method they have until after they file a claim. By then, it may be too late to make changes.

Arkansas Roof Coverage Rules Matter

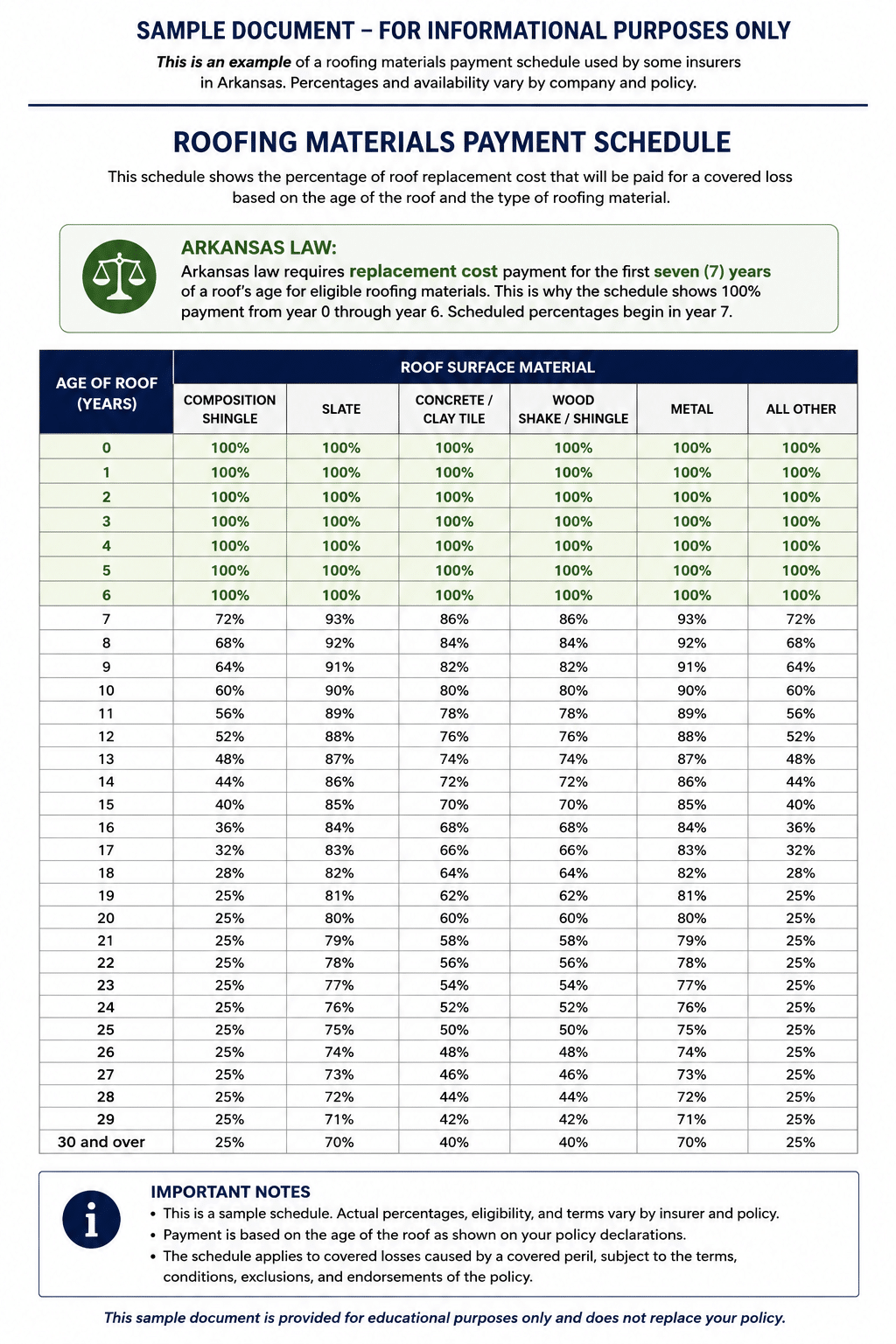

Under current Arkansas rules for qualifying homeowners policies, covered roof losses may receive replacement cost treatment during the first seven years of a roof’s life. That is why many Arkansas roof payment schedules begin with 100% payment through years 0–6, with scheduled payment percentages beginning in year 7.

Arkansas Roofs Face Some of the Toughest Weather in America

Hail

Even small hail can bruise shingles, damage roof vents, and reduce the life of your roof.

High Wind

Arkansas experiences damaging straight-line winds and tornado-related storms every year.

Aging Roofs

As roofs age, insurance companies often change how claims are settled and how coverage is offered.

The Three Ways Roof Claims Are Commonly Paid

Before you can decide whether Replacement Cost or an Agreed Roof Payment Schedule is better, you first need to understand how each roof settlement method works.

Replacement Cost

Replacement Cost is designed to pay the cost to replace damaged roofing materials with similar new materials, subject to your deductible, policy limits, and policy conditions.

This is often the strongest option for newer roofs, but it does not mean every roof claim automatically results in a full roof replacement.

Actual Cash Value

Actual Cash Value, often called ACV, usually means the claim payment is reduced for depreciation based on the roof’s age, condition, and useful life.

ACV can result in a much lower claim payment, especially on older composition shingle roofs.

Agreed Roof Payment Schedule

An Agreed Roof Payment Schedule uses a set percentage listed in the policy based on roof age and roof material.

Instead of waiting until after the claim to learn how depreciation may apply, the schedule shows the percentage in advance.

| Coverage Type | How It Usually Works | Main Benefit | Important Limitation |

|---|---|---|---|

| Replacement Cost | Pays to replace covered damaged roofing materials with similar new materials. | Can provide the highest claim payment for qualifying roof losses. | Still subject to policy language, exclusions, roof condition, deductible, and claim investigation. |

| Actual Cash Value | Pays replacement cost minus depreciation. | May reduce premium compared with broader roof settlement options. | Older roofs may receive a much smaller payout. |

| Agreed Roof Payment Schedule | Pays a predetermined percentage based on roof age and material. | The settlement percentage is shown before the loss occurs. | The scheduled percentage may be lower than full replacement cost on older roofs. |

Key Point

Replacement Cost may sound better, but the real question is whether your roof will qualify for full replacement cost benefits after a loss. For older roofs, an Agreed Roof Payment Schedule may create clearer expectations because the payout percentage is shown in the policy before the claim happens.

Why Arkansas Roof Payment Schedules Often Start at 100%

One of the most important things Arkansas homeowners need to understand is that roof payment schedules do not always begin reducing the roof payment immediately.

Arkansas Rules Can Protect Newer Roofs

Under current Arkansas rules for qualifying homeowners policies, covered roof losses may receive replacement cost treatment during the first seven years of the roof’s life.

That is why many Arkansas roof payment schedules show 100% payment from year 0 through year 6. The scheduled percentages often begin in year 7.

This matters because some homeowners see the words “roof payment schedule” and assume the policy immediately becomes a low-value roof policy. In Arkansas, that is not always the case. For qualifying roof losses during the first seven years, the schedule may still show 100%.

After year 7, the scheduled percentage may depend on the age of the roof and the type of roofing material. Composition shingles, slate, metal, concrete tile, clay tile, wood shake, and other roof materials may all have different scheduled percentages.

Sample Arkansas Roofing Materials Payment Schedule

The sample below is recreated for educational purposes only. It is not tied to any specific insurance company and should not be used as a substitute for your actual policy.

Example: How a Schedule May Change by Roof Age

Here is a simplified example using a composition shingle roof. Actual schedules vary by insurer, policy, roof material, endorsements, and eligibility.

| Roof Age | Example Scheduled Payment | What It Means |

|---|---|---|

| 0–6 Years | 100% | Replacement cost treatment may apply for qualifying covered roof losses during the first seven years. |

| 7 Years | 72% | The roof begins settling according to the schedule. |

| 10 Years | 60% | The payout is based on the listed percentage, not a new depreciation decision after the claim. |

| 15 Years | 40% | The homeowner should understand the expected payout before a storm happens. |

| 20+ Years | 25% | The scheduled payout may be lower, but it is more predictable than waiting for depreciation to be determined after the loss. |

Important Reminder

A roof payment schedule does not mean every roof claim will automatically be paid. The loss still must be caused by a covered peril and must satisfy the terms, conditions, exclusions, and endorsements of the policy.

Why an Agreed Roof Payment Schedule May Actually Be Better

This is one of the biggest misconceptions we see when reviewing homeowners insurance policies. Most people assume that Replacement Cost is always the best roof coverage. For many newer roofs, that can be true. However, for some older roofs, an Agreed Roof Payment Schedule may provide a more predictable claim experience.

Replacement Cost Does Not Automatically Mean a New Roof

One of the most common misunderstandings in homeowners insurance is believing that having Replacement Cost coverage automatically guarantees a full roof replacement after every storm. It does not. Every claim must still satisfy the terms, conditions, exclusions, endorsements, and settlement provisions contained in the policy.

Replacement Cost

Replacement Cost can provide outstanding protection for newer roofs. However, every claim is still evaluated according to the policy. Examples of factors that may affect claim handling include:

- Cause of loss

- Roof condition before the storm

- Maintenance history

- Existing deterioration

- Prior repairs

- Policy exclusions

- Roof settlement endorsements

- Applicable policy conditions

Agreed Roof Payment Schedule

With an Agreed Roof Payment Schedule, the settlement percentage is established before the loss occurs. Instead of waiting until after a storm to determine how depreciation or settlement will be calculated, the policy contains a published payment schedule based on roof age and roof material.

- Known payment percentages

- Predictable settlement method

- No surprises about scheduled payment percentages

- Often available for older roofs

Real World Example

Scenario A

Your home has a five-year-old architectural shingle roof. A severe hailstorm causes widespread covered damage. Because the roof is relatively new, Replacement Cost coverage may provide the greatest financial protection, subject to the policy’s terms and conditions.

Scenario B

Your home has an eighteen-year-old roof. You already know your policy’s published payment schedule. Rather than wondering how the roof settlement percentage may be determined after a covered loss, you understand the scheduled percentage before the storm ever happens.

The Best Roof Coverage Depends on Your Roof

There is no one-size-fits-all answer. The right roof coverage depends on roof age, roof material, roof condition, budget, insurance company, policy language, and your tolerance for financial risk.

At Cribb Insurance Group, we believe homeowners should understand how their roof will be settled before they ever have to file a claim.

How Much Could Your Roof Claim Be Worth?

Percentages are helpful, but most homeowners want to know what those percentages actually mean in dollars. The following examples are for educational purposes only and assume a covered loss before deductible.

| Estimated Roof Replacement Cost | Replacement Cost | Actual Cash Value* | Example Scheduled Payment at 60% |

|---|---|---|---|

| $15,000 | $15,000 | $8,000–$11,000 | $9,000 |

| $25,000 | $25,000 | $13,000–$18,000 | $15,000 |

| $40,000 | $40,000 | $20,000–$28,000 | $24,000 |

*Actual Cash Value examples are simplified estimates for illustration only. Actual depreciation varies by roof age, condition, material, insurer, and policy language.

Notice Something Interesting?

Many homeowners automatically assume an Agreed Roof Payment Schedule will always pay less than every other settlement method. That is not necessarily true. For some older roofs, an Actual Cash Value settlement may produce a payment that is similar to—or even lower than—a scheduled payment.

The important point is understanding how your specific policy settles roof claims before a storm happens.

The Right Question Is Not “Which Coverage Is Cheapest?”

The better question is:

“Which roof settlement method gives me the protection and predictability I want?”

That answer may be different for a five-year-old roof than it is for an eighteen-year-old roof.

Questions Every Arkansas Homeowner Should Ask Before Renewing Their Policy

The best time to understand your roof coverage is before a storm—not after you file a claim. Use these questions when reviewing your homeowners policy or shopping for insurance.

Is my roof covered by Replacement Cost, Actual Cash Value, or a Roof Payment Schedule?

Do not assume you have Replacement Cost simply because someone told you that years ago. Review your current policy to verify how roof losses are settled.

What happens after my roof reaches seven years old?

Ask whether your policy changes how roof claims are settled after year seven and whether a payment schedule applies.

Does my policy include cosmetic damage limitations?

Some policies treat cosmetic roof damage differently than functional damage. Make sure you understand how your policy responds.

Does roof condition affect claim eligibility?

Understanding how your insurer evaluates roof condition before a loss can help avoid surprises during the claims process.

How much is my roof deductible?

Know whether your deductible is a flat dollar amount or a percentage of your home’s insured value.

Does my policy include matching coverage?

Ask how your policy handles situations where damaged shingles cannot be matched to the existing roof.

How old is my roof according to my insurance company?

The age your insurer has on file may not always match your expectations. Verify that your records are accurate.

Should I replace my roof before shopping for insurance?

Depending on your roof’s age and condition, replacing the roof before changing insurance companies may improve available coverage options.

Can another insurance company offer better roof coverage?

Independent insurance agencies can compare multiple carriers to help determine which companies provide the coverage that best fits your home.

Not Sure How Your Roof Is Covered?

Our licensed Arkansas insurance advisors can review your current homeowners policy, explain how your roof is covered, compare multiple insurance companies, and help you understand your options before your next renewal.

Common Myths About Roof Insurance in Arkansas

There is a lot of misinformation online about roof insurance. Here are some of the biggest myths we hear every day—and the facts every Arkansas homeowner should know.

Replacement Cost Always Means You Will Receive a Brand-New Roof

Many homeowners believe that seeing “Replacement Cost” on their policy guarantees a full roof replacement after every storm.

Roof Payment Schedules Are Always Bad

Many homeowners immediately reject any policy with a Roof Payment Schedule.

Actual Cash Value and Roof Payment Schedules Are the Same Thing

Although both may reduce claim payments compared to Replacement Cost, they work differently.

Older Roofs Cannot Be Insured

Many homeowners think that once their roof reaches a certain age, they cannot obtain homeowners insurance.

Every Insurance Company Handles Roof Claims the Same Way

Coverage can vary significantly from one insurer to another.

Frequently Asked Questions About Roof Insurance in Arkansas

These are some of the most common questions Arkansas homeowners ask us when reviewing their homeowners insurance.

Does Arkansas require Replacement Cost on roofs?

What happens after my roof turns seven years old?

Is Replacement Cost always the best coverage?

Is an Agreed Roof Payment Schedule the same as Actual Cash Value?

Can my insurance company deny my roof claim because my roof is old?

Does hail always require a new roof?

What is cosmetic roof damage?

Should I replace my roof before changing insurance companies?

How can I find out which roof settlement option I have?

Can Cribb Insurance compare multiple companies for roof coverage?

Helpful Cribb Insurance Resources

Want to learn more about insurance in Northwest Arkansas? Visit our home insurance page, explore insurance options in Bentonville, Rogers, and Fayetteville, or read our Arkansas home insurance cost guide.

Know How Your Roof Is Covered Before the Next Storm

Most homeowners do not find out how their roof claim will be settled until after hail, wind, or storm damage has already happened.

At Cribb Insurance Group, we review more than just price. We help Arkansas homeowners understand roof settlement options, deductibles, endorsements, exclusions, payment schedules, and carrier differences before they need to file a claim.