Last updated: May 2026

Written by Cribb Insurance Group

Serving Bentonville, Rogers, Fayetteville, Springdale, Bella Vista, Centerton, Siloam Springs, and homeowners across Northwest Arkansas

If you’ve recently purchased a home, received a renewal notice, or started comparing insurance quotes, you’re probably asking the same question many Arkansas homeowners are asking right now:

How much does homeowners insurance cost in Arkansas?

As of 2026, the average homeowners insurance cost in Arkansas ranges from approximately $3,700 to $5,000 per year, depending on your home’s value, roof age, location, deductible, and claims history.

Homeowners in Northwest Arkansas cities like Bentonville, Rogers, and Fayetteville often pay higher-than-average premiums because of tornado, hail, and severe storm risk.

For a typical $400,000 home in Northwest Arkansas, annual premiums commonly range from $2,000 to $5,000+, depending on the carrier, deductible structure, and coverage selections.

The good news? Rates can vary dramatically between insurance companies — sometimes by thousands of dollars per year for the exact same home.

This guide breaks down:

- Average home insurance rates in Arkansas

- Why premiums have increased

- What affects your rate

- How Northwest Arkansas compares

- How to lower your homeowners insurance costs

Key Takeaways

- Arkansas homeowners insurance rates are among the highest in the United States.

- Most Arkansas homeowners pay between $3,700 and $5,000 annually for coverage.

- Tornadoes, hailstorms, and severe weather are major drivers of rising premiums.

- Many policies now include percentage-based wind and hail deductibles.

- Shopping multiple insurance carriers can save homeowners thousands per year.

- Roof age, credit score, claims history, and dwelling coverage all heavily affect pricing.

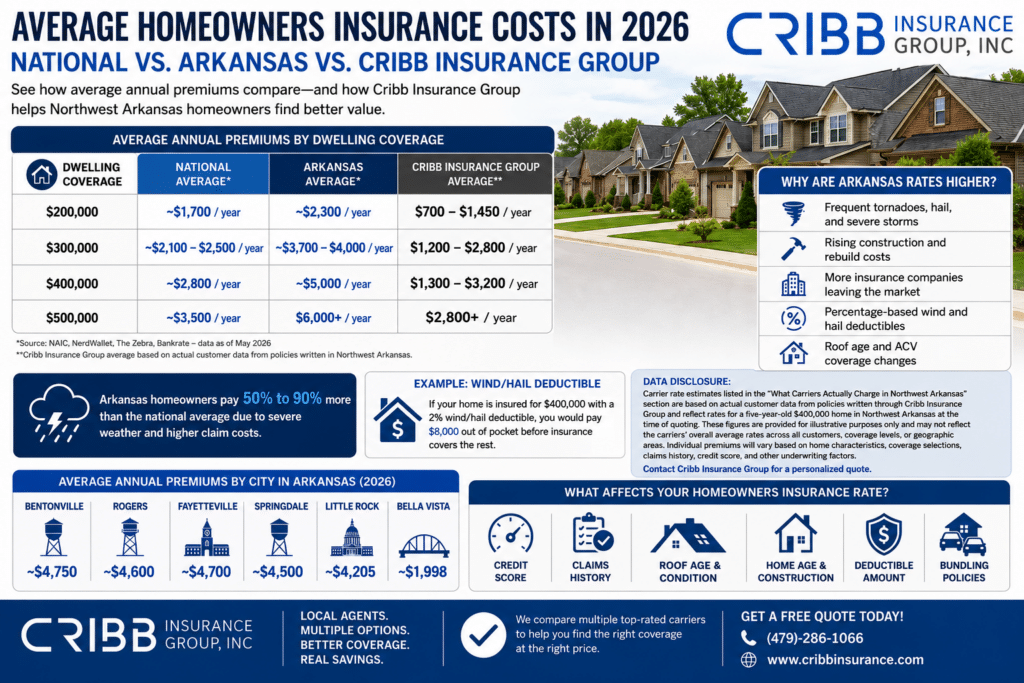

Average Homeowners Insurance Cost in Arkansas vs. National Average (2026)

Here’s how Arkansas compares to national averages for homeowners insurance in 2026:

| Dwelling Coverage | Arkansas Average | National Average |

|---|---|---|

| $200,000 | ~$2,300/year | ~$1,700/year |

| $300,000 | ~$3,700–$4,000/year | ~$2,100–$2,500/year |

| $400,000 | ~$5,000/year | ~$2,800/year |

| $500,000 | $6,000+/year | ~$3,500/year |

Arkansas homeowners typically pay 50% to 90% more than the national average because of the state’s high frequency of tornadoes, hailstorms, and wind-related insurance claims.

According to the National Association of Insurance Commissioners (NAIC), the average U.S. homeowners insurance premium ranges from approximately $2,100 to $2,543 annually for a home with $300,000 in dwelling coverage.

Why Is Homeowners Insurance So Expensive in Arkansas?

Several major factors have pushed Arkansas homeowners insurance rates higher over the past several years.

1. Severe Weather and Tornado Risk

Arkansas sits in one of the most active severe weather regions in the country.

According to the National Oceanic and Atmospheric Administration (NOAA), Arkansas experiences approximately 40 tornadoes annually, with peak activity typically occurring between March and June.

Hailstorms, straight-line winds, and tornado outbreaks generate massive insurance losses statewide.

Northwest Arkansas is heavily affected.

In May 2024, seven confirmed tornadoes struck Benton and Madison counties during a single severe weather outbreak, damaging or destroying hundreds of homes across the region.

Insurance companies price premiums based on risk exposure and claims history. When severe storms generate large losses year after year, premiums increase across the market.

2. Rising Construction and Rebuild Costs

Home repair and rebuilding costs have increased substantially over the past several years.

Labor shortages, material inflation, roofing costs, and supply chain disruptions have all contributed to higher replacement costs for homes.

This affects homeowners insurance directly because policies are designed to cover the cost to rebuild your home — not necessarily what you originally paid for it.

Many Arkansas homeowners may now be underinsured if their dwelling coverage hasn’t been updated recently.

3. Insurance Companies Leaving the Arkansas Market

The Arkansas property insurance market has become increasingly difficult for carriers.

Industry analyses show some Arkansas property insurers operating with loss ratios exceeding 100%, meaning companies are paying out more in claims than they collect in premiums.

Several carriers have reduced exposure or exited the Arkansas market entirely.

Fewer carriers competing in the state often means:

- higher premiums

- stricter underwriting

- fewer coverage options

- tighter roof restrictions

4. Percentage-Based Wind and Hail Deductibles

Arkansas recently allowed broader use of split deductibles for wind and hail claims.

Instead of a flat deductible like $1,000 or $2,500, many policies now use a percentage-based deductible tied to your dwelling coverage amount.

For example:

- Home insured for $400,000

- 2% wind/hail deductible

- Out-of-pocket responsibility = $8,000 before insurance coverage begins

This is one of the most important coverage changes Arkansas homeowners should understand today.

5. Roof Age and Agreed Roof Schedule Coverage

Many carriers now use an agreed roof schedule for older roofs rather than offering full replacement cost coverage.

Under these policies, the amount paid for roof damage is based on a predetermined coverage schedule tied to the roof’s age and condition.

For example, a 10-year-old roof damaged by hail may only qualify for a percentage of the replacement cost, depending on the insurer’s roof schedule.

Roof age has become one of the most important underwriting and pricing factors in Arkansas homeowners insurance.

Average Homeowners Insurance Costs by City in Arkansas

Insurance premiums vary significantly across Arkansas depending on weather exposure, claims history, fire protection ratings, and home values.

| City | Average Annual Premium |

|---|---|

| Bentonville | ~$4,750/year |

| Rogers | ~$4,600/year |

| Fayetteville | ~$4,700/year |

| Springdale | ~$4,500/year |

| Little Rock | ~$4,205/year |

| Bella Vista | ~$1,998/year |

Bella Vista consistently ranks among the more affordable areas in Arkansas for homeowners insurance.

Bentonville and Fayetteville typically see higher premiums due to:

- rising home values

- rapid growth

- increased rebuild costs

- severe weather exposure

What We’re Seeing in Northwest Arkansas

At Cribb Insurance Group, we’ve seen many Northwest Arkansas homeowners experience premium increases of 20% to 40% over the past several years — especially on homes with:

- older roofs

- prior claims

- lower deductibles

- aging electrical or plumbing systems

We’re also seeing major differences between carriers for identical homes.

In some cases, one carrier may quote $2,000 per year while another quotes over $5,000 for nearly the same coverage.

That’s why comparing multiple insurance companies matters more today than ever before.

Real Homeowners Insurance Rates in Northwest Arkansas

The following examples reflect actual premium ranges from carriers partnered with Cribb Insurance Group for a five-year-old $400,000 home in Northwest Arkansas.

| Carrier | Estimated Annual Premium | Notes |

|---|---|---|

| Cincinnati Insurance | ~$1,362/year | Auto bundle required |

| Acuity | ~$1,568/year | Auto bundle required |

| National General | ~$2,170/year | Bundled rate |

| The Hartford | ~$2,250/year | Bundled rate |

These examples illustrate how dramatically rates can vary between insurance companies.

The right carrier could potentially save a Northwest Arkansas homeowner thousands of dollars annually for comparable coverage.

What Affects Your Homeowners Insurance Premium?

Several personal and property-specific factors influence what you’ll pay for home insurance in Arkansas.

Credit Score

Credit is one of the most influential pricing factors in Arkansas insurance markets.

Homeowners with excellent credit often pay significantly lower premiums than homeowners with poor credit histories.

Improving your credit score can substantially reduce your insurance costs over time.

Claims History

Frequent claims typically lead to higher premiums.

Filing multiple small claims may cost more in long-term premium increases than the claim payout itself.

Roof Age

Older roofs are more expensive to insure because they are more vulnerable to wind and hail damage.

Many carriers apply:

- roof surcharges

- ACV settlements

- coverage limitations

- inspection requirements

once roofs reach certain age thresholds.

Home Age and Construction Type

Older homes with:

- outdated wiring

- aging plumbing

- older HVAC systems

- original roofs

usually cost more to insure.

Newer homes built with modern building codes and storm-resistant materials often qualify for lower rates.

Deductible Choice

Higher deductibles generally reduce your annual premium.

Moving from a $2500 deductible to a $2% deductible can meaningfully lower your monthly insurance costs.

Bundling Home and Auto Insurance

Bundling policies with the same carrier can often reduce premiums by 15% to 35%.

This remains one of the easiest ways to lower overall insurance costs.

What Does Homeowners Insurance Cover?

A standard HO-3 homeowners insurance policy typically includes:

- Dwelling coverage

- Other structures coverage

- Personal property protection

- Liability insurance

- Additional living expenses (ALE)

What Is Usually NOT Covered?

Most standard homeowners insurance policies do not automatically cover:

- Flood damage

- Earthquake damage

- Sewer backup

- Certain roof exclusions

- Some cosmetic hail damage

Flood insurance requires a separate policy through either:

- the National Flood Insurance Program (NFIP)

- or a private flood insurance carrier

Homeowners Insurance in Bentonville and Rogers

Bentonville and Rogers homeowners have seen rising insurance costs because of:

- rapidly increasing property values

- population growth

- severe weather exposure

- higher rebuild costs

Newer homes may qualify for discounts if they include:

- impact-resistant roofing

- modern electrical systems

- storm-resistant construction materials

- monitored security systems

Even within the same city, ZIP-code-level claims history can significantly affect rates.

How to Lower Your Homeowners Insurance Premium in Arkansas

Arkansas homeowners can often reduce insurance costs using several practical strategies.

1. Shop Multiple Carriers

Rates vary dramatically between insurance companies.

Comparing quotes through an independent insurance agency can uncover major savings opportunities.

2. Bundle Home and Auto Policies

Bundling remains one of the fastest ways to reduce total insurance costs.

3. Improve Your Credit Score

Better credit frequently leads to better insurance pricing.

4. Review Your Dwelling Coverage

Make sure your dwelling coverage reflects current rebuild costs — not your home’s purchase price.

5. Consider a Higher Deductible

If financially comfortable, increasing your deductible can lower premiums substantially.

6. Upgrade Your Roof

New roofs often qualify for improved pricing and broader coverage options.

7. Avoid Small Claims

Maintaining a clean claims history helps preserve lower rates long-term.

Why Work With an Independent Insurance Agent?

Independent insurance agencies can compare multiple carriers instead of offering only one company’s products.

That matters in Arkansas because:

- coverage restrictions vary widely

- roof guidelines differ significantly

- wind/hail deductibles vary by carrier

- pricing differences can be substantial

At Cribb Insurance Group, we help Northwest Arkansas homeowners compare:

- premiums

- deductibles

- roof coverage

- endorsements

- exclusions

- carrier financial strength

so homeowners can make informed decisions based on both price and protection.

Frequently Asked Questions About Homeowners Insurance in Arkansas

What is the average homeowners insurance cost in Arkansas in 2026?

Most Arkansas homeowners pay between $3,700 and $5,000 annually in 2026 depending on coverage amount, roof age, claims history, deductible structure, and location.

Why is homeowners insurance so expensive in Arkansas?

Arkansas experiences frequent tornadoes, hailstorms, severe thunderstorms, and wind claims, which drive higher insurance losses and premiums.

Does homeowners insurance cover tornado damage?

Yes. Standard homeowners insurance policies generally cover tornado and wind damage, subject to deductibles and policy limits.

What is a wind and hail deductible?

A wind and hail deductible is the amount you must pay out of pocket before insurance coverage begins for storm-related claims.

Many Arkansas policies now use percentage-based deductibles.

Does homeowners insurance include flood insurance?

No. Flood insurance requires a separate policy.

How often should I shop homeowners insurance?

Most homeowners should compare rates every 12–24 months, especially after:

- major premium increases

- roof replacements

- home renovations

- severe weather events

Ready to Compare Homeowners Insurance Rates in 2026?

If you haven’t reviewed your homeowners insurance recently, there’s a good chance your rates, deductibles, or coverage options have changed.

Cribb Insurance Group helps homeowners throughout Northwest Arkansas compare multiple carriers and understand their options clearly.

Whether you live in:

- Bentonville

- Rogers

- Fayetteville

- Springdale

- Bella Vista

- Centerton

- Siloam Springs

our team can help you evaluate pricing, coverage, deductibles, and policy structure based on your specific home and needs.

Get a Free Quote

🌐 www.cribbinsurance.com

📞 Contact Cribb Insurance Group to compare homeowners insurance quotes from multiple carriers in Northwest Arkansas.

Data sources referenced include the National Association of Insurance Commissioners (NAIC), National Oceanic and Atmospheric Administration (NOAA), NerdWallet, The Zebra, Bankrate, Arkansas Insurance Department, and regional reporting from Northwest Arkansas news organizations.

**Data Disclosure: Carrier rate estimates listed in the “What Carriers Actually Charge in Northwest Arkansas” section are based on actual customer data from policies written through Cribb Insurance Group and reflect rates for a five-year-old $400,000 home in Northwest Arkansas at the time of quoting. These figures are provided for illustrative purposes only and may not reflect the carriers’ overall average rates across all customers, coverage levels, or geographic areas. Individual premiums will vary based on home characteristics, coverage selections, claims history, credit score, and other underwriting factors. Contact Cribb Insurance Group for a personalized quote.